- Harbourfront Quantitative Newsletter

- Posts

- Identifying and Characterizing Market Regimes Across Asset Classes

Identifying and Characterizing Market Regimes Across Asset Classes

A Regime-Switching Framework for Foreign Exchange Hedging and Equity Market Analysis

Nam Nguyen

October 12, 2025 • Estimated Reading Time: 5 minutes

Identifying market regimes is essential for understanding how risk, return, and volatility evolve across financial assets. In this edition, we examine two quantitative approaches to regime detection. Together, these studies highlight how data-driven frameworks can improve both risk management and trading performance.

In this issue:

Latest Posts

The Role of Data in Financial Modeling and Risk Management (13 min)

Volatility Risk Premium Across Different Asset Classes (13 min)

When Trading Systems Break Down: Causes of Decay and Stop Criteria (12 min)

Volatility Targeting Across Asset Pricing Factors and Industry Portfolios (12 min)

Tail Risk Hedging Using Option Signals and Bond ETFs (12 min)

Wall Street Isn’t Warning You, But This Chart Might

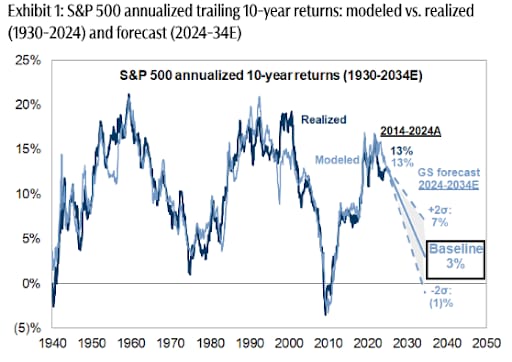

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

Hedge Effectiveness Under a Four-State Regime Switching Model

Identifying market regimes is important for understanding shifts in risk, return, and volatility across financial assets. With the advancement of machine learning, many regime-switching and machine learning methods have been proposed. However, these methods, while promising, often face challenges of interpretability, overfitting, and a lack of robustness in real-world deployment.

Reference [1] proposed a more “classical” regime identification technique. The authors developed a four-state regime switching (PRS) model for FX hedging. Instead of using a simple constant hedge ratio, they classified the market into regimes and optimized hedge ratios accordingly.

Findings

The study develops a four-state regime-switching model for optimal foreign exchange (FX) hedging using forward contracts.

Each state corresponds to distinct market conditions based on the direction and magnitude of deviations of the FX spot rate from its long-term trend.

The model’s performance is evaluated across five currencies against the British pound over multiple investment horizons.

Empirical results show that the model achieves the highest risk reduction for the US dollar, euro, Japanese yen, and Turkish lira, and the second-best performance for the Indian rupee.

The model demonstrates particularly strong performance for the Turkish lira, suggesting greater effectiveness in hedging highly volatile currencies.

The model’s superior results are attributed to its ability to adjust the estimation horizon for the optimal hedge ratio according to current market conditions.

This flexibility enables the model to capture asymmetry and fat-tail characteristics commonly present in FX return distributions.

Findings indicate that FX investors use short-term memory during low market conditions and long-term memory during high market conditions relative to the trend.

The model’s dynamic structure aligns with prior research emphasizing the benefits of updating models with recent data over time.

Results contribute to understanding investor behavior across market regimes and offer practical implications for mitigating behavioral biases, such as panic during volatile conditions.

In short, the authors built a more efficient hedging model by splitting markets into four conditions instead of two, adjusting hedge ratios and memory length depending on the volatility regime. This significantly improves hedge effectiveness, especially in volatile currencies.

We believe this is an efficient method that can also be applied to other asset classes, such as equities and cryptocurrencies.

Reference

[1] Taehyun Lee, Ioannis C. Moutzouris, Nikos C. Papapostolou, Mahmoud Fatouh, Foreign exchange hedging using regime-switching models: The case of pound sterling, Int J Fin Econ. 2024;29:4813–4835

Using the Gaussian Mixture Models to Identify Market Regimes

Reference [2] proposed an approach that uses the Gaussian Mixture Models to identify market regimes by dividing it into clusters. It divided the market into 4 clusters or regimes,

Cluster 0: a disbelief momentum before the breakout zone,

Cluster 1: a high unpredictability zone or frenzy zone,

Cluster 2: a breakout zone,

Cluster 3: the low instability or the sideways zone.

Findings

Statistical analysis indicated that the S&P 500 OHLC data followed a Gaussian (Normal) distribution, which motivated the use of Gaussian Mixture Models (GMMs) instead of k-means clustering, since GMMs account for the distributional properties of the data.

Traditional trading strategies based on the Triple Simple Moving Average (TSMA) and Triple Exponential Moving Average (TEMA) were shown to be ineffective across all market regimes.

The study identified the most suitable regimes for each strategy to improve portfolio returns, highlighting the importance of regime-based application rather than uniform use.

This combined approach of clustering with GMM and regime-based trading strategies demonstrated potential for improving profitability and managing risks in the S&P 500 futures market.

In short, the triple moving average trading systems did not perform well. However, the authors managed to pinpoint the market regimes where the trading systems performed better, relatively speaking.

Reference

[2] F. Walugembe, T. Stoica, Evaluating Triple Moving Average Strategy Profitability Under Different Market Regimes, 2021, DOI:10.13140/RG.2.2.36616.96009

Closing Thoughts

Both studies underscore the importance of regime identification and adaptive modeling in financial decision-making. The four-state regime-switching hedging model demonstrates how incorporating changing market conditions enhances risk reduction in foreign exchange markets, while the Gaussian Mixture Model approach illustrates how clustering can effectively capture distinct market phases in equity trading. Together, they highlight the value of data-driven, regime-aware frameworks in improving both risk management and trading performance.

Educational Video

In this video, quantitative analyst Alis Angello interviews Dr. Edward Tsang, a pioneer in applying AI to finance since the 1980s. Dr. Tsang explains how his work on directional change and hidden Markov models helps identify market regimes, distinguishing normal and volatile periods. By feeding minute-level market data into machine learning algorithms, these models classify patterns and recognize regime shifts in real time, allowing traders to react quickly and reduce drawdowns.

Dr. Tsang notes that his students have successfully extended these ideas into industry applications, often keeping their methods proprietary. He emphasizes that his published research demonstrates proof of concept, showing that incorporating regime recognition improves performance even with simple strategies. He also discusses how AI is used more broadly in finance, referencing his book AI for Finance, which provides a high-level overview of real-world applications.

In the conversation, he cautions that regulators still prefer transparent, simple models for compliance purposes, while firms can use more complex AI internally for simulation, portfolio optimization, and stress testing. Throughout the discussion, Dr. Tsang underscores the importance of understanding both theory and practicality—designing algorithms that not only detect market patterns but also align with institutional and regulatory constraints.

Most coverage tells you what happened. Fintech Takes is the free newsletter that tells you why it matters. Each week, I break down the trends, deals, and regulatory shifts shaping the industry — minus the spin. Clear analysis, smart context, and a little humor so you actually enjoy reading it.

Volatility Weekly Recap

The figure below shows the term structures for the VIX futures (in colour) and the spot VIX (in grey).

The equity market opened the week in the green, then retreated on Tuesday, but reached an all-time high again on Wednesday. On Thursday, the market reversed, and then turned truly bearish on Friday as new concerns about potential international trade tensions swept through. Overall, the S&P 500 fell 2.43% and the Nasdaq lost 2.53%. Oil prices rose early in the week but fell significantly heading into the weekend. Gold continued to soar, jumping another 1.9% for the week. Bitcoin made a new all-time high before pulling back sharply on Friday alongside the rest of the market.

On the volatility front, spot VIX rose significantly above 21%, and VIX futures also increased. The roll yield decreased, closing near zero. Despite the rise in both spot and VIX futures, the term structure remained fairly flat, i.e., neither in strong backwardation nor deep contango.

Around the Quantosphere

Big Dollar Short Becoming the Pain Trade for Investors (advisorperspectives)

Hedge Funds Back Year-End Dollar Rally With Options Bets (bloomberg)

Preparing for Growth: How Emerging Hedge Fund Managers Can Use Risk Management as a Competitive Advantage (hedgeweek)

How multi-million pay packages killed a small London hedge fund (reuters)

More Google engineers are being tempted away to prop trading firms (efinancialcareers-canada)

Systematic Hedge Funds Hit With Daily Losses in October, Says Goldman (reuters)

AI Drives Surge in WorldQuant’s University Enrollment (yahoo finance)

Human vs Machine: Who Wins in the World of Funds Management? (afr)

Hedge Funds Targeting Fire Insurance Hit a Wall in California (yahoo finance)

Disclaimer

This newsletter is not investment advice. It is provided solely for entertainment and educational purposes. Always consult a financial professional before making any investment decisions.

We are not responsible for any outcomes arising from the use of the content and codes provided in the outbound links. By continuing to read this newsletter, you acknowledge and agree to this disclaimer.