- Harbourfront Quantitative Newsletter

- Posts

- Effectiveness of Covered Call Strategy in Developed and Emerging Markets

Effectiveness of Covered Call Strategy in Developed and Emerging Markets

Risk–Return Trade-Offs in Covered Call Strategies

Nam Nguyen

October 19, 2025 • Estimated Reading Time: 5 minutes

Covered call strategies are often promoted as an income-generation tool for investors seeking steady returns with reduced risk. But how effective are they in practice? In this issue, we take a closer look at their real-world performance across different markets.

In this issue:

Latest Posts

Identifying and Characterizing Market Regimes Across Asset Classes (13 min)

The Role of Data in Financial Modeling and Risk Management (13 min)

Volatility Risk Premium Across Different Asset Classes (13 min)

When Trading Systems Break Down: Causes of Decay and Stop Criteria (12 min)

Volatility Targeting Across Asset Pricing Factors and Industry Portfolios (12 min)

Like Moneyball for Stocks

The data that actually moves markets:

Congressional Trades: Pelosi up 178% on TEM options

Reddit Sentiment: 3,968% increase in DOOR mentions before 530% in gains

Plus hiring data, web traffic, and employee outlook

While you analyze earnings reports, professionals track alternative data.

What if you had access to all of it?

Every week, AltIndex’s AI model factors millions of alt data points into its stock picks.

We’ve teamed up with them to give our readers free access for a limited time.

The next big winner is already moving.

Past performance does not guarantee future results. Investing involves risk including possible loss of principal.

Do Covered Calls Deliver Superior Returns?

The covered call strategy is a popular and conservative options trading approach. It involves an investor holding a long position in an underlying asset, typically a stock, and then selling call options on that asset. These call options provide the buyer with the right to purchase the underlying asset at a predetermined strike price within a specific timeframe. By selling these calls, the investor generates additional income through the premiums received.

While the covered call strategy provides an additional income, it caps potential profits if the asset’s price rises significantly. Covered calls are often employed by investors seeking income while holding a moderately bullish view of the underlying asset’s price. It can be an effective way to enhance returns and manage risk in a portfolio.

The investment management industry has actively promoted the covered call strategy. But in reality, does it deliver superior returns compared to the buy-and-hold approach? Reference [1] effectively examined this question.

Findings

The study evaluates the performance of a covered call strategy relative to the SPY ETF benchmark over the period from July 2009 to April 2023.

Three covered call variations are analyzed: at-the-money (ATM), two percent out-of-the-money (OTM), and five percent OTM call options.

The results show no statistically significant difference between the covered call strategies and the benchmark in terms of overall performance.

Among the tested strategies, the five percent OTM covered call achieved the highest annualized return of 16%, followed by the two percent OTM with 15%, compared to SPY’s 13%.

The study cautions investors that these figures do not account for taxes, transaction costs, or implementation expenses, which could reduce the strategy’s real-world profitability.

The analysis distinguishes between two major market periods — the COVID-19 pandemic and the Russia–Ukraine conflict — to evaluate performance consistency.

The findings suggest that while covered call strategies may offer comparable or slightly better returns in some conditions, their advantage is not statistically robust.

The thesis excludes mean-variance ratios due to potential biases caused by the negatively skewed return distribution of covered call strategies.

The results imply that covered call strategies may be better suited for specific market environments rather than as a general outperforming strategy.

Overall, the study highlights the limited evidence supporting the superiority of covered call strategies over a simple buy-and-hold approach for ETFs.

Reference

[1] Tomáš Ježo, Effect of covered calls on portfolio performance, 2023, Charles University

Do Covered Calls Deliver Superior Returns – Emerging Markets

The previous paper discussed the risk-adjusted returns of the covered call strategy in the US market. Reference [2] further studied the profitability of the covered call strategy in international markets.

Findings

The study evaluates the effect of call writing on ETF portfolio returns and risk, focusing on the Indian capital market.

Results indicate that adding call writing to ETFs generally reduces returns and increases risk compared to holding ETFs alone.

Exceptions occur for portfolios using deep out-of-the-money (OTM) options—specifically OTM5 and OTM7—which achieved higher returns but also significantly higher risk.

The OTM5 portfolio showed a 47% gain in rupee terms and 27% as a percentage of investment, though its risk nearly doubled.

The high volatility of options often leads to sharp losses, with the potential to erase a year’s gains in a single week of negative returns.

ETFs, while index-based, do not perfectly track their benchmarks, contributing to deviations in portfolio performance.

The higher return of the OTM5 portfolio is attributed to a 68% success rate, suggesting potential benefits if the strategy is applied consistently over the long term.

The findings support the idea that covered call strategies can generate income and manage risk if applied using deep OTM options and maintained for extended periods.

The study aligns with prior research indicating that covered call strategies underperform in bull markets but can reduce risk or outperform in neutral or declining markets.

In brief, in the Indian market, covered calls yield lower returns with higher risks (as measured by portfolio volatility). The exception is when selling far out-of-the-money call options, but even then, the risk-adjusted returns remain lower due to the higher volatility of returns. This result is consistent with the result in the US market.

Reference

[2] Dr. Abhishek Shahu1, Dr. Himanshu Tiwari, Dr. Mahesh Joshi, Dr. Sanjay Kavishwar, An Analysis of the Effectiveness of Index ETFS and Index Derivatives in Covered Call Strategy, Journal of Informatics Education and Research, Vol 4 Issue 3 (2024)

Closing Thoughts

Both studies assess covered call strategies and reach broadly consistent conclusions. The U.S. study finds only marginal performance improvements over buy-and-hold, while the emerging market study shows potential for higher returns using deep out-of-the-money options but at increased risk. Overall, covered calls may enhance income under specific market conditions, though their benefits remain limited and context-dependent.

Educational Video

Covered Calls: The Income Illusion

In this video, portfolio manager Ben Felix from PWL Capital critiques the widespread appeal of covered call funds, arguing that their high-income appearance results from product design rather than superior performance. He explains that while covered calls generate option premiums distributed as income, these premiums are offset by the loss of upside potential. The illusion of stable income, combined with mental accounting biases, makes the strategy appear more profitable than it truly is.

Felix notes that conventional risk-adjusted metrics like the Sharpe ratio fail to account for skewness introduced by options, leading to misleadingly strong results. When properly adjusted for these distortions—as well as for taxes, fees, and implementation costs—covered call strategies tend to underperform simple stock index investments over time.

Toward the end, Felix includes insights from academics Meir Statman and Campbell Harvey, who both emphasize behavioral and statistical misconceptions driving investor enthusiasm for covered calls. Together, they reinforce Felix’s central argument that covered call funds appeal to cognitive biases rather than sound portfolio theory and that, in most cases, their perceived advantage is an income illusion rather than a genuine improvement in returns.

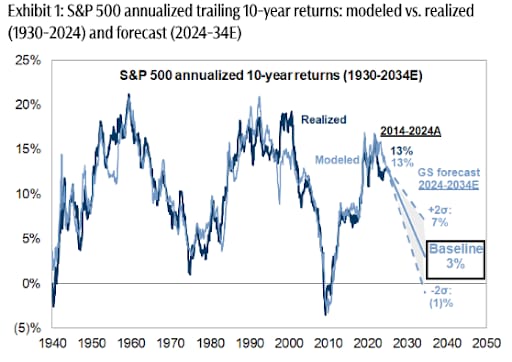

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

Volatility Weekly Recap

The figure below shows the term structures for the VIX futures (in colour) and the spot VIX (in grey).

Following the plunge last Friday, the market bounced at Monday’s open on hopes that the selloff was overdone. On Wednesday, strong earnings reports from the banking sector brought bullish sentiment back, but on Thursday, new disclosures from regional banks regarding bad loans weighed on stocks. On Friday, the market was range-bound in the morning but staged a moderate rally into the close. The S&P 500 gained 1.7%, and the Nasdaq rose 2.14% for the week.

Oil prices came under pressure from renewed tariff tensions; despite a significant drop on Friday, gold managed to reach a new all-time high during the week. Bitcoin and the rest of the crypto market sold off, finishing the week deep in the red.

On the volatility front, compared to last week’s close, levels did not change much, but the front end of the spot and futures curves moved into slight backwardation. Despite this, both VXX and VIXM posted negative returns. The roll yield shifted from positive to slightly negative.

Around the Quantosphere

Hedge Funds Stay Defensive as Retail Traders Buy Every Dip (hedgeweek)

AI Disruption Arrives in Asset Management (yahoo finance)

The quants who built computer-run trading strategies aren't ready to hand it over to AI (yahoo finance)

Man Group’s $214 Billion Comeback: Hedge Fund Giant Turns Tariff Turmoil Into Triumph (yahoo finance)

JPMorgan Says Native Traders Drove the Crypto Crash (cryptopolitan)

Ken Griffin Says GenAI Fails to Help Hedge Funds Produce Alpha (bloomberg)

Why even top quant graduates are still struggling to get jobs (efinancialcareers-canada)

Hedge Funds Pile into Once-Esoteric Commodity Curve Option Bets (bloomberg)

No One Slept That Night: How Hedge Funds Rode Out Crypto’s Darkest Weekend (fnlondon)

Disclaimer

This newsletter is not investment advice. It is provided solely for entertainment and educational purposes. Always consult a financial professional before making any investment decisions.

We are not responsible for any outcomes arising from the use of the content and codes provided in the outbound links. By continuing to read this newsletter, you acknowledge and agree to this disclaimer.